For businesses that generate revenue from long-term contracts, accurate revenue recognition is crucial for producing reliable financial statements. This is particularly important in industries like software and construction, where contracts can last several months or even years. The timing of revenue recognition is vital, often determined by the start and end dates of the contracts, which affect how revenue is reported over time. Given that many mid-market businesses do not accurately track long-term contract revenue, this becomes a core focus during business transaction due diligence.

Understanding the Revenue Recognition Principle

Revenue recognition is a key aspect of accrual accounting that determines when and how businesses record their revenue. Businesses must select the method that best reflects their performance obligations under the contract. For long-term contracts, this principle is generally governed by two methods:

- Percentage-of-Completion Method: Revenue is recognized progressively over the life of the contract, based on the proportion of work completed.

- Completed Contract Method: Revenue is only recognized once the entire contract is completed.

Start Date: The Trigger for Revenue Recognition

Revenue recognition begins when a business starts fulfilling its obligations under a contract. This does not always coincide with the contract signing date but instead begins when actual work or services commence. Depending on the industry and the type of contract, this could mean the start of a design phase, initiation of construction, or delivery of a key service.

Tracking Progress: The Importance of Milestones and Timeframes

For long-term contracts, especially those with multiple phases or milestones, accurate measurement of progress is critical. Businesses typically use either input measures (e.g., costs incurred, or hours worked) or output measures (e.g., units delivered, or milestones achieved) to determine how much revenue to recognize over the life of the contract. For example, in software contracts, progress would be measured by the time elapsed over the service delivery period. In the case of an annual contract, this would imply revenues recognized over a 12-month period irrespective of whether payment is received upfront.

End Date: Closing the Revenue Cycle

The contract’s end date is another critical factor in revenue recognition. For businesses using the completed contract method, all revenue is deferred until the end of the contract. Only once the business has fulfilled all obligations, and the contract is formally concluded, can they recognize any revenue. This is especially important in industries where contract terms can change or extend, potentially pushing revenue recognition further out than initially planned.

Even under the percentage of completion method, businesses must ensure that all performance obligations are met before recognizing final revenues. Any work not yet completed by the end date can lead to adjustments, deferred revenue, or even losses if cost overruns occur.

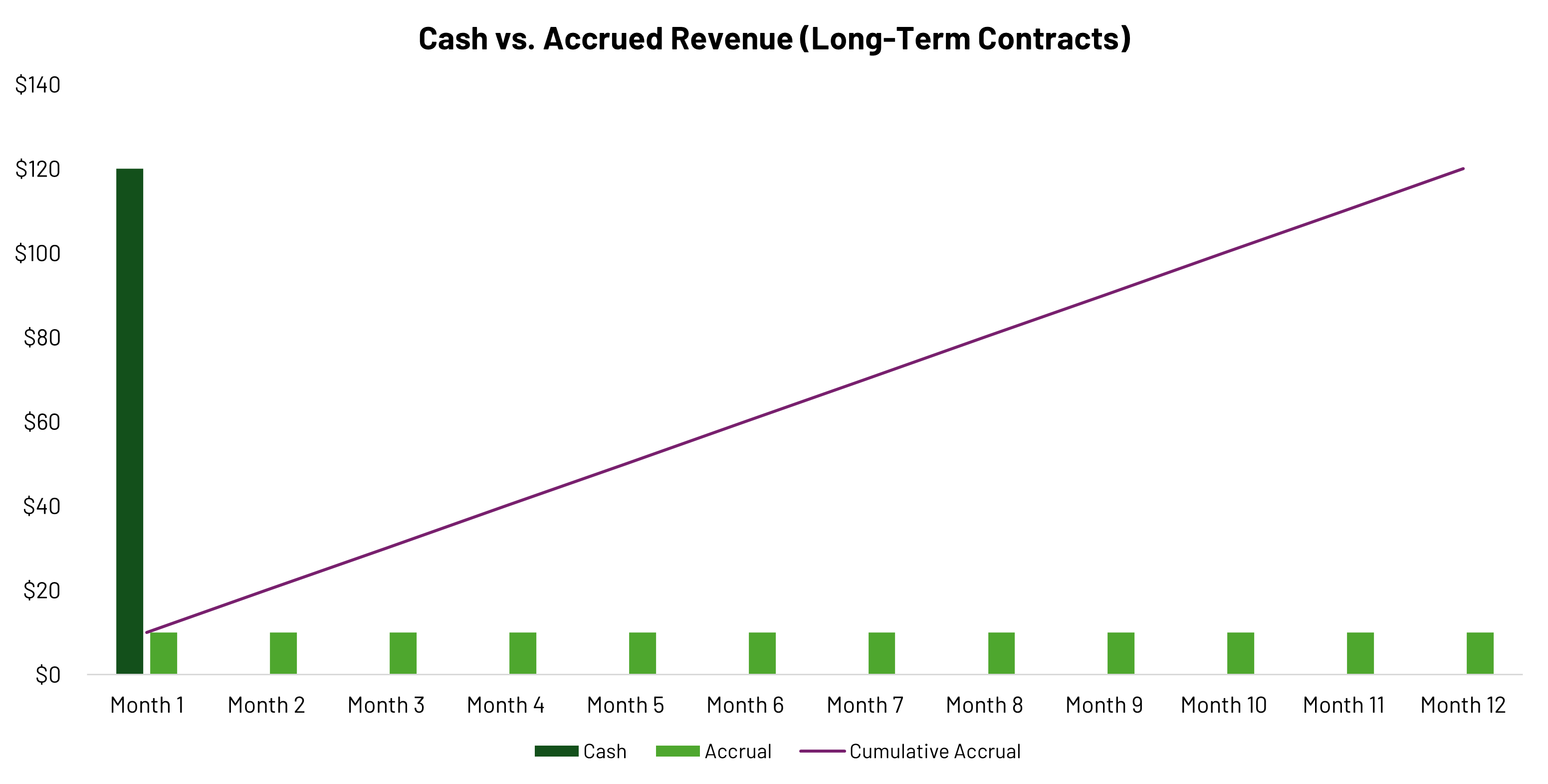

Exhibit1: Example of a 12-month contract showing the actual cash inflow versus the methodology for recognition in the financial statements.

Revenue Recognition Standards (ASC 606/IFRS 15)

The adoption of Accounting Standards Codification 606 (“ASC 606”) for US GAAP and International Financial Reporting Standard (“IFRS15”) has brought about significant changes in revenue recognition practices. These standards emphasize recognizing revenue as a company fulfills its performance obligations, aligning revenue recognition more closely with contract progress. For long-term contracts, this means determining the specific obligations tied to the start and end dates and recognizing revenue as these are satisfied.

Case Study: Software-as-a-Service Client of Sapling

An example of such a case was a Quality of Earnings engagement conducted by Sapling. The target company was a vertical market software-as-as-service business with revenues of $15 million. Deferred the revenue calculated by the company did not account for the day in the month on which the contract started, tracking progress on a monthly basis rather than daily. This resulted in overstated revenues and understated deferred revenue. Sapling restated this company’s revenues and deferred revenues resulting in an approximate $100K difference in their deferred revenue estimate, which was important for determining the appropriate working capital adjustment to the deal value.

Final Thoughts

For businesses with long-term contracts, accurate revenue recognition is crucial for properly reflecting financial performance. The start and end dates of contracts are more than just administrative details—they play a central role in determining when and how much revenue a business can recognize. By aligning revenue recognition methods with the progress of contract fulfillment, companies can ensure that their financial reporting remains accurate and compliant.