The most intense M&A negotiations usually occur when the purchase price is the focus of the discussion. This is especially true when dealing with items that can lead to a price adjustment after closing the transaction. When a buyer agrees to purchase a business from a seller, they expect the business to be delivered with a certain level of net working capital (“NWC”). This amount is the targeted net working capital, also known as the NWC peg.

The M&A negotiation process can be lengthy, and during this time the target’s working capital may fluctuate due to cyclical factors. This fluctuation may disproportionately favour the buyer or seller, so one way to mitigate it is to agree on an NWC peg. The common practice is to take the average of the trailing twelve months (“TTM”) of the target’s NWC as this smooths out variance and gives a reasonable estimate for future working capital needs.

What is Net Working Capital (NWC)?

In its most basic definition, working capital is the difference between Current Assets and Current Liabilities. Current Assets represent liquid assets, either cash or resources that can be turned into cash within a year (e.g., Accounts Receivable and Inventory). On the other hand, Current Liabilities are obligations that need to be serviced within a year (e.g., Accounts Payable).

When working capital is positive, it means that the business has enough liquid assets to be able to meet its short-term obligations. When negative, the business may need to rely on short-term draws such as working capital facilities to satisfy its obligations.

In an M&A negotiation, the determination of the NWC peg is a key point of dispute. This is because the difference between the target net working capital and the actual net working capital delivered at closing will lead to a purchase price adjustment for the transaction.

Determining the NWC Peg

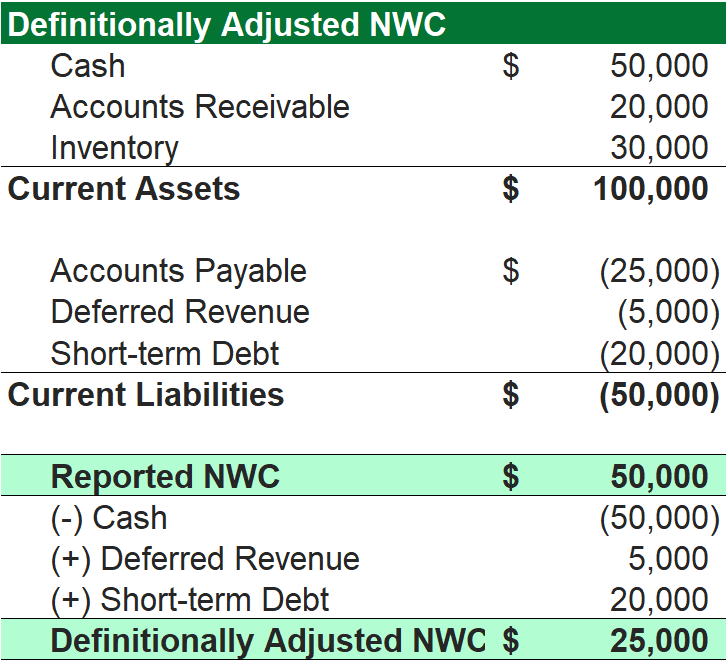

The starting point for the calculation of the NWC peg is the basic definition of NWC (i.e., Current Assets less Current Liabilities). From there, the reported net working capital is adjusted for definitional terms. The NWC peg only considers operating items to be representative of the core business. For this reason, certain non-operating current assets and current liabilities are removed from the calculation. On the asset side, this includes cash and cash equivalents like short-term investments. Many M&A deals are done on a cash-free, debt-free basis, and these items are generally not required to run the core business. Similarly, obligations like short-term loans are excluded.

After excluding the non-operating items, the result is the definitionally adjusted NWC. Up to this point, the buyer and seller are generally in agreement with the calculation, as the adjustments tend to be difficult to argue. From here, negotiations usually determine how remaining items in NWC should be treated. One of the biggest discussion points here is on the treatment of deferred revenue.

Exhibit 1: Definitionally Adjusted NWC

Deferred Revenue Treatment

Deferred revenue is formally defined as a current liability and is created when a business collects cash upfront for revenue it will deliver in the future. In many cases, deferred revenue is treated as short-term debt as it is an obligation that the buyer will need to fulfill upon acquiring the business. On the other hand, it may be argued that it is only partially an obligation. In these cases, only the cost to service the deferred revenue based on the target’s gross margins may be treated as short-term debt and excluded from the NWC peg calculation.

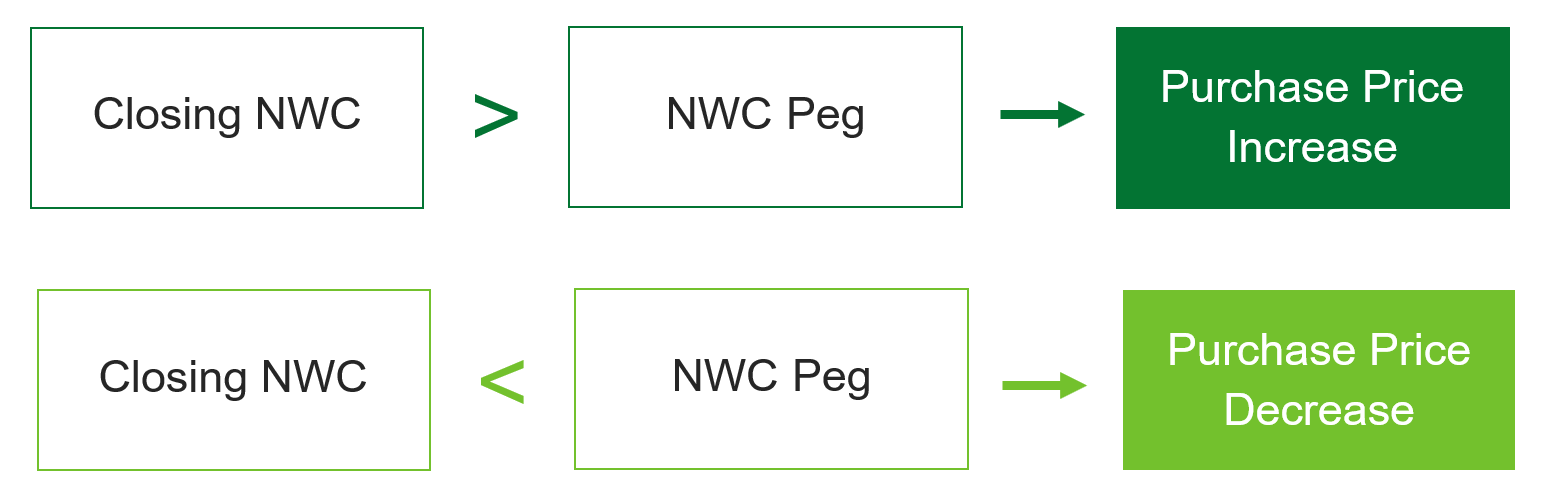

The key point of disagreement here is usually not on whether deferred revenue should be included but rather how much should be removed. This is where the buyer and seller each try to tilt the scales in their favour. Going back to the definition of the NWC peg: since this represents the amount of NWC that the buyer is expected to deliver, the higher it is, the less likely they are to meet the threshold at closing. Buyers benefit from a higher NWC peg as it increases the likelihood that the actual NWC will be lower than the targeted NWC, which results in a downward purchase price adjustment. This situation implies that the buyer may need to use external funding to be able to sustain ongoing operations.

On the other hand, the seller favours a lower NWC peg. This increases the likelihood that the actual NWC will be higher than the targeted NWC at closing. If this happens, then the excess is treated as an amount that is not needed to operate the business and should be returned to the seller, increasing the purchase price through an upward purchase price adjustment.

Exhibit 2: Purchase Price Adjustment

Since deferred revenue is a current liability, its exclusion benefits the buyer since it raises the NWC, and the buyer would always prefer if the full amount were excluded since this maximizes the amount of the downward adjustment. The seller tends to push back on the amount of deferred revenue that should be excluded. If only the cost to service the debt is excluded, then the scales tilt in the seller’s favour since it lowers the amount of the upward adjustment.

Conclusion

The NWC peg is just one part of the M&A process, and its calculation should usually be validated through a detailed quality of earnings review. In the end, both parties should arrive to a fair target that can be clearly communicated in the share purchase agreement. As one of the main considerations in the purchase price adjustment, it’s important that both sides do their due diligence to minimize surprises after closing.