Quality of Earnings (QoE) reports are essential for both buyers and sellers in a transaction. For buyers seeking to acquire companies with lower EBITDA, a comprehensive QoE report and databook may not be economical. In this case, a cash proof analysis of the target may be sufficient, depending on the buyer’s due diligence objectives. A cash proof analysis validates reported financial statements by proving that net income turns into cash.

Components of a Cash Proof

At a high level, a cash proof analysis provides validation that reported net income and EBITDA produce cash, as well as shows the main sources and uses of cash. The cash proof analysis can be separated into three sections: the reconciliation of net income to net bank deposits, the reconciliation of sales to bank deposits, and the reconciliation of expenses to bank disbursements.

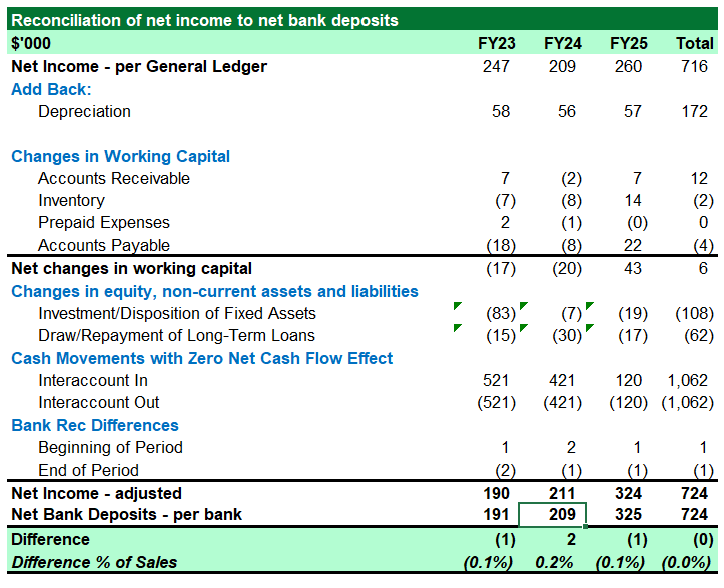

- Reconciliation of Net Income to Net Bank Deposits

This section reconciles reported net income to the net change in bank balances by adjusting for non-cash items, changes in working capital, and non-operating and financing activities (See Exhibit A). The purpose is to demonstrate that reported profitability translates into actual cash and that there are no unexplained differences between earnings and cash.

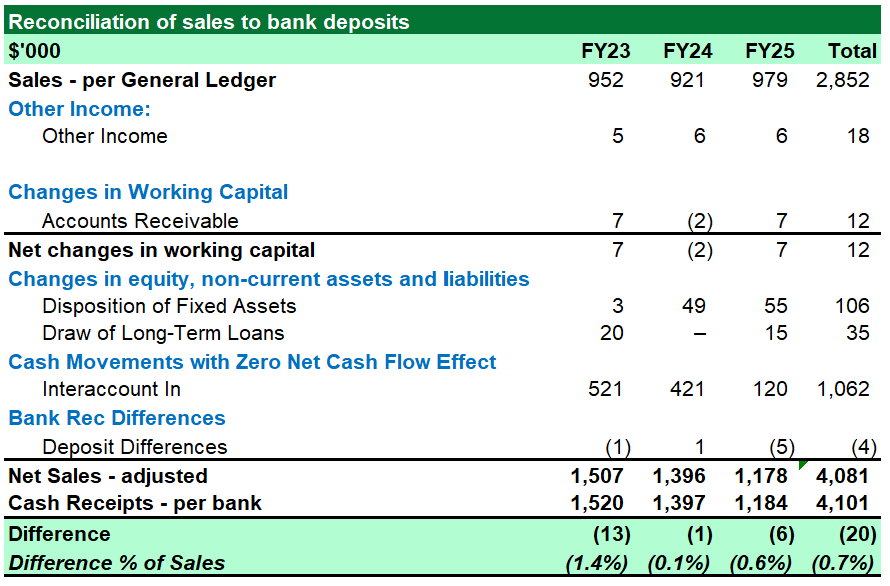

- Reconciliation of Sales to Bank Deposits

The sales to bank deposits reconciliation ties reported revenue to cash received by adjusting for timing differences, such as accounts receivable and deferred revenue, and any non-cash items (See Exhibit B). It is meant to validate the existence of revenue by showing that reported revenue turns into cash.

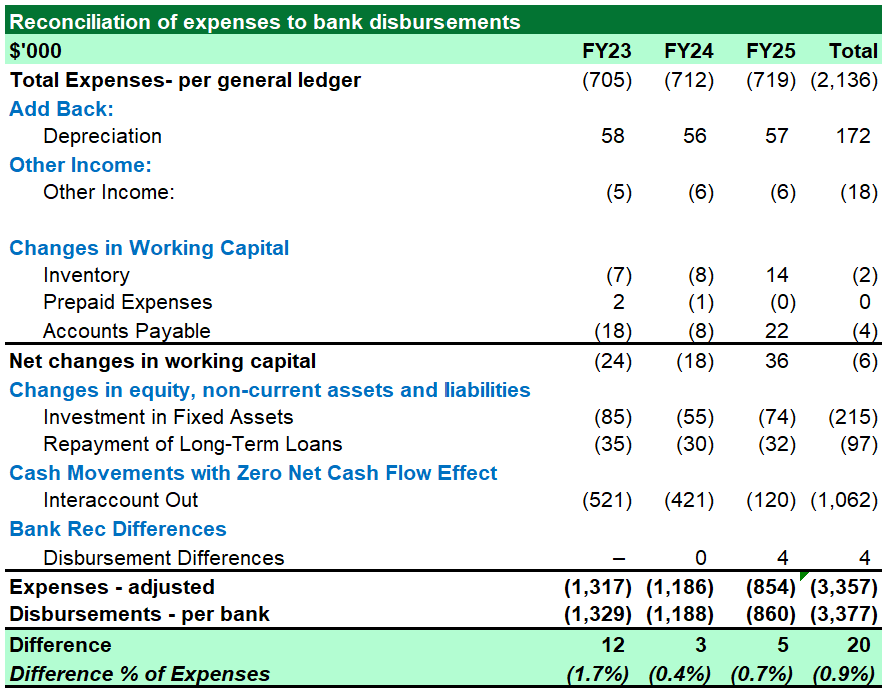

- Reconciliation of Expenses to Bank Disbursements

This section links reported expenses to cash payments made from bank accounts, with adjustments made for movements in expense-related working capital items, non-cash charges, and financing activities (See Exhibit C). The objective is to confirm that cash outflows support reported expenses.

When Does a Cash Proof Make Sense

For company’s with complex business models with multiple revenue streams, legal/reporting entities, deferred revenue streams, or any material unexplained expenses, a QoE report provides buyers with the confidence to identify trends in revenue streams, understand revenue drivers, ensure that all revenue is recorded in the correct period, and gain clarity on whether all expenses are recurring and necessary to the business. Along with the QoE report, a cash proof analysis can further validate the target’s EBITDA by comparing the reported income statement against inflows and outflows from the bank statements. This gives buyers confidence that they are not overpaying for a company with an inflated EBITDA due to an increase in reported revenue without receiving cash.

Even when acquiring a company with a simpler business model where a full QoE report, including adjustments and revenue analysis, may seem unnecessary, getting a cash proof analysis of the target still gives the buyer confidence that the reported financial statements reflect the underlying operation of the business by showing that net income translates into cash inflows in the company’s bank accounts.

Conclusion

While judgment needs to be made in every scenario, when a target has a simple business model and lower EBITDA, buyers can benefit from a cash proof analysis, rather than a full QoE report, to decrease costs, while still validating the target’s EBITDA and cash flow.

Exhibit A: Reconciliation of Net Income to Net Bank Deposits

Exhibit B: Reconciliation of Sales to Bank Deposits

Exhibit C: Reconciliation of Expenses to Bank Disbursements