Capital budgeting is the process of evaluating and selecting large and long-term investments that demand significant capital, including but not limited to the purchase of a new facility, fixed assets, machinery or equipment. While large enterprises often have the resources to conduct detailed analyses, small to medium-sized enterprises (“SMEs”) often lack the necessary resources to perform a proper capital budgeting process and either use a simplified process or rely on the owner’s intuition to make these critical business decisions, which could result in making a poor investment decision. This blog post explores how SMEs can best approach the capital budgeting process with the minimal resources they have.

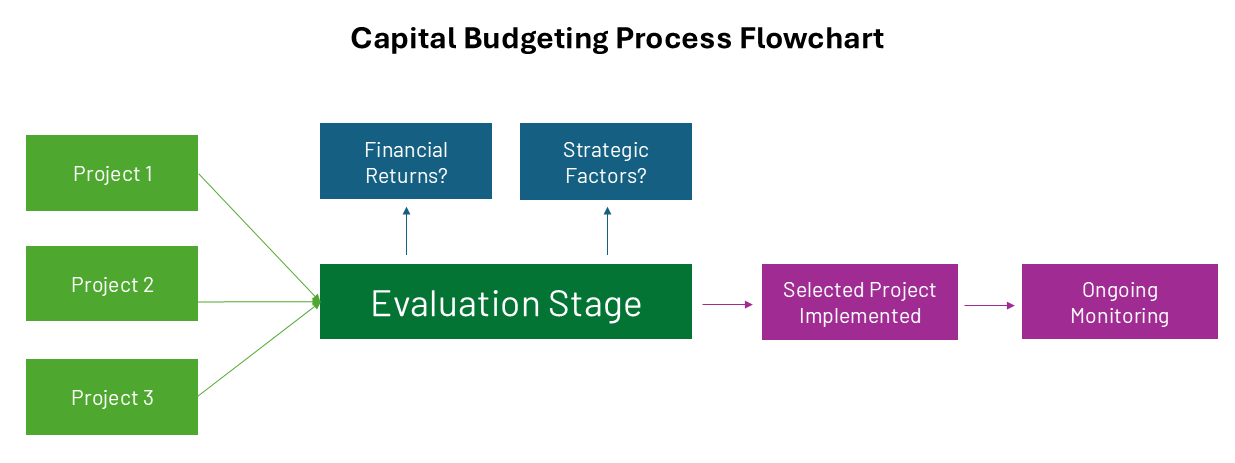

Capital Budgeting Process

Project Generation: The first step in the Capital Budgeting process is to source potential projects from various departments, with potential key benefits, incremental cash flow and financing methods.

Evaluate the proposals: Next, each proposal needs to be evaluated both quantitively and qualitatively. Projects need fit to the business’s strategic goals and generate sufficient financial returns. The fundamental approach to evaluating the proposals from a financial standpoint is as follows:

- Identify the initial capital expenditures and the associated setup costs.

- Calculate proposed cash inflows or expense savings from the proposed project.

- Determine how the project should be financed, typically this will either come from internal financing by improving operating efficiencies or equity financing. Due to the size of SMEs and traditional banks’ low appetite for risk, debt financing such as bank loans is often less accessible for riskier projects, including investments in new, unproved technologies.

- Establish the measurement used to evaluate the project. The most common ones include payback period, the Net Present Value (“NPV”) and the Internal Rate of Return (“IRR”). SMEs typically prefer the payback period due to its simplicity to execute & understand. However, the simple payback period often excludes the time value of money, which is a key factor in the capital budgeting process that could hinder the accuracy of the analysis.

Select a project: Consider various factors, including the business model, industry trends, macro trends, and financial outcomes of different projections.

Project implementation & ongoing review: Execute the planned investment, monitor the operational and financial performance, and make necessary adjustments to ensure alignment with strategic goals and optimal resource utilization.

Exhibit 1: Visualization of the entire capital budgeting process

The benefit of Capital Budgeting for SMEs

- Get better deals on fixed assets: By doing proper projections and analysis, business owners can step into the negotiation phase with better insights about the value of the fixed asset, avoiding the situation of overpaying for an asset which can not be justified with its the underlying benefits. A common example is when a business purchases a fixed asset at a price that exceeds the net discounted differential cash flow it generates.

- Save money on long-term projects: Building a capital budget helps SMEs to understand their cash needs and avoid unexpected liquidity shortfalls, which can lead to the use of high-interest debt or missed payment penalties.

- Improve financial stability & profitability: Planning for upcoming capital expenditures encourages business owners to re-invest cash generated during operations into the company to create further value rather than making distributions, which may prevent the business from reaching its full potential.

Unique challenges SMEs face during Capital Budgeting

- The volatility and/or availability of historical financials: Capital budgeting is most effective when there’s a track record of stable financials to base projections on. However, given SMEs tend to experience notable volatility in historical financials, making it more challenging to generate reliable forecasts.

- Financing considerations: The access to capital, particularly through traditional bank loans, is more limited for SMEs. Therefore, SMEs often need to look further into internal financing, typically by optimizing working capital, or other alternative financing methods to secure financing needs for any capital expenditures.

Although SMEs may have minimal resources and face unique challenges in the capital budgeting process, implementing a structured, quantitative-based approach can help them make more informed investment decisions and optimize their resources. By carefully evaluating projects, considering financing options, and using appropriate financial metrics, SMEs can enhance their financial stability and long-term profitability. A well-executed capital budgeting process empowers SMEs to allocate capital efficiently, mitigate risks, and drive sustainable growth.