For M&A transactions structured on a cash-free, debt-free basis, a net debt analysis helps buyers and sellers understand how the agreed enterprise value translates into the actual equity value paid at closing. Since enterprise value assumes the business is transferred without excess cash or outstanding debt, a net debt analysis helps to identify which balance sheet items should be treated as debt-like, cash-like, or included in normal working capital. This is important because every item classified as debt-like reduces the seller’s proceeds, while every item classified as cash-like increases the seller’s proceeds, directly impacting the final purchase price.

Unlike items such as accounts receivable or inventory, indebtedness in an M&A context is not always defined by IFRS or any other single accounting standard. Beyond traditional bank debt, buyers often look at liabilities or obligations that are financing-like, non-operating, non-recurring, overdue, or not already reflected in normalized working capital or EBITDA. Since these items require judgement, buyers and sellers can take different views on how the same balance sheet item should be treated, which is why net debt is often one of the key areas of negotiation in the purchase agreement.

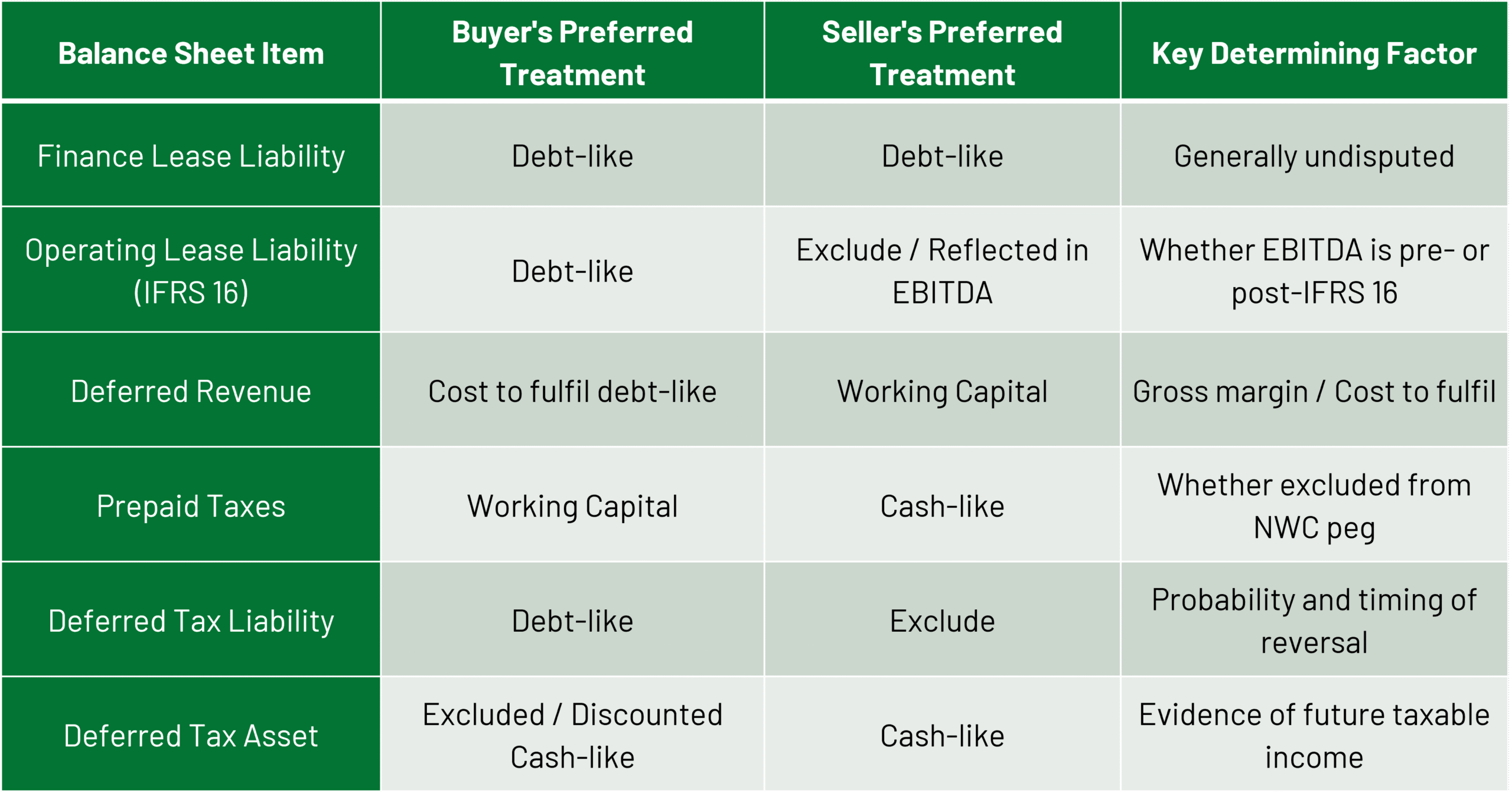

Commonly Disputed Items

The following items are frequently subject to disagreement between buyers and sellers in net debt negotiations (see Exhibit A):

- Leases: Under IFRS 16, most leases are now recognized on the balance sheet as Right-Of-Use (ROU) assets with corresponding lease liabilities. On one hand, buyers want to treat lease liabilities as debt-like, especially where EV/EBITDA multiples are based on post-IFRS 16 EBITDA. On the other hand, sellers usually push back and argue for rent costs that are already reflected in the earnings used to value the business. One important note is that if EBITDA is presented pre-IFRS 16, including the lease liability in net debt would result in double-counting. Under US GAAP, ASC 842, leases also need to be accounted for in the balance sheet with finance and operating leases generating ROU assets and their respective lease liabilities. The main distinction arises from the way they are presented in the income statement. Finance leases are accounted for similar to how it is done under IFRS 16, wherein depreciation and interest expense are included below EBITDA. This makes it easier to consider financing lease accounting as debt-like. But operating leases still need to be reported as one straight-line lease expense above EBITDA since the rent expense is already included in EBITDA.

Under ASPE, the accounting treatment of leasing resembles that IAS 17 (predecessor to IFRS 16) lease standard in terms of having two different classifications of leases – capital and operating leases. Capital leases are recorded in the balance sheet, and the associated obligation can be considered as debt in terms of net debt calculation. In turn, operating leases do not affect the balance sheet of a company, and neither ROU asset nor a lease obligation is recorded in this case. Consequently, operating leases of companies using ASPE accounting are not included in the net debt calculation while the rent expense is an operating expense above EBITDA. However, it may be worth reviewing off-balance sheet lease obligations indicated in the notes in order to identify any material lease obligations to include in the net debt schedule.

- Deferred Revenue: Buyers view deferred revenue as a future service obligation that will require the business to incur costs to fulfil and therefore argue for debt-like treatment. On the other side, sellers argue deferred revenue is a working capital item reflecting cash collection timing. In this case, the appropriate treatment depends on the gross margin of the underlying service. The debate is usually not whether the full deferred revenue balance is debt-like, but whether the cost to fulfil the obligation should be treated as debt-like or captured in working capital.

- Prepaid Taxes: A prepaid tax balance represents tax instalments paid in excess of the current liability, which generates a refund receivable from the tax authority. Sellers seek to recognize confirmed, near-term refunds as cash-like items, whereas buyers often treat these as working capital. The key question is whether the amount is recoverable and whether it has already been included in the normalized working capital peg. If it is excluded from the peg and expected to convert into cash, sellers may argue for cash-like treatment.

- Deferred Tax Assets and Liabilities: A deferred tax liability (DTL) represents future tax outflows and is generally treated as a debt-like item where reversal within the investment horizon is probable. A deferred tax asset (DTA) is only treated as cash-like where future taxable income to absorb it is well-supported by projections. Where utilization is uncertain, advisors will typically apply a discount or exclude the DTA balance entirely.

Conclusion

Regardless of whether an item is treated as debt-like, cash-like, or included in working capital, the classification has a direct impact on the equity value paid at closing. Generally, buyers are motivated to identify items as debt-like because they reduce the purchase price, while sellers often argue that these items should be captured in working capital to preserve the proceeds. Having an unbiased advisor apply a consistent classification across the net debt schedule helps both parties support their position and reach a fair outcome during negotiation.

Exhibit A: Net Debt Classification Summary